Risk and Renewables

- Ali Ahmed

- Oct 9, 2020

- 3 min read

Three risk factors driving the rise in renewable energy and one still holding it back.

Most discussions of renewable energy and its ever increasing adoption on a global scale focus on technology and cost. However, if you consider renewable energy in terms of business risk, the decision to select renewable energy becomes even more compelling whether you are a generator, a utility, or a consumer.

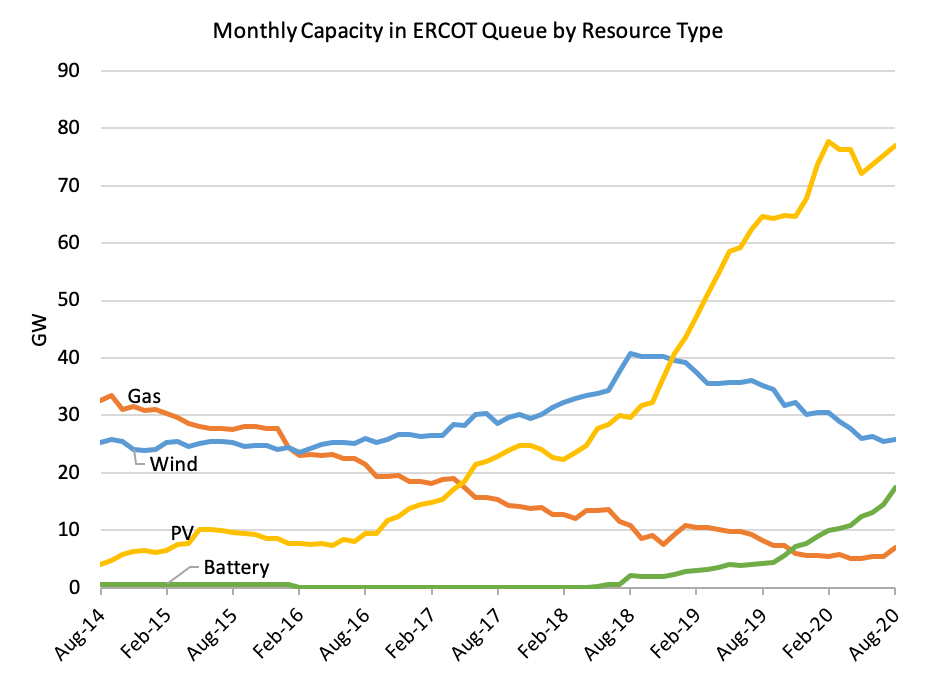

The risks and the way businesses look at the risk associated with renewable energy have dramatically dropped, particularly in comparison with fossil fuel options, which is continuing to drive selection of renewables. A recent study from the Rocky Mountain Institute clearly shows this shift with renewable energy options far exceeding fossil fuels in the power capacity construction pipeline in Texas. The significant increase in battery capacity, bolstered by the latest FERC Order 2222 which increasingly opens markets to distributed energy resources (DER), will further support this trend.

The underlying risk factor becoming more widely understood and accepted is the production risk, i.e. how much energy will the generation system produce. Traditional utilities and fossil-based energy companies have long disparaged renewables as 'intermittent' and 'unreliable' sources of energy. In real-time, this is correct, but in longer horizons - those matching the investment horizons made by generation companies and energy consumers - renewables are extremely predictable. We have excellent climate models which predict how much wind and sun will be available at a location, and we now have real world examples of operational systems that validate these models. We have also seen an increase in system reliability to the point that generators are even willing to make production guarantees to customers. In contrast, the increase in severe weather events is making the availability of fossil fuels more risky. Weather events including not just hurricanes but also severe cold can have a significant impact on production, consumption, and pricing (EIA, Factors affecting natural gas pricing).

The second driving factor is lower marginal price risk. There is no fuel cost for the wind and the sun, but fossil fuel generation pricing is heavily linked to fuel cost. In 2018, fuel costs for US investor owned electric utility generating plants was over 70% of total operating expense for fossil steam plants and over 80% for natural gas turbine plants (EIA, Electric Power Annual). This makes fossil fuels a much riskier option since any event that causes fuel prices to change is highly impactful.

These two risk factors coupled with the continuing improvements in technology have led to the third factor, reduction of financing risk, the ability of an energy project to raise capital and the interest rate of that capital. The improved perception and track record of existing projects is minimizing the risk premium that investors were requiring previously. Coupled with the dramatic rise in socially conscious or ESG investment preferences, the total cost of capital for creating new renewable energy is extremely low. Significant amounts of low cost capital and large investors actively seeking projects will continue to increase the pipeline of new renewable energy projects.

So what continues to hold back this shift in energy production? In many regions, public utility commissions which regulate investor owned utilities have an antiquated methodology for rate setting based on pre-established rates of return on capital investments. This means that in many situations where utilities are making investment choices for new generation or distribution systems to better support renewable energy, risk is not a factor. The rate of return is guaranteed and all the risk is born by the consumers on their bills with items like 'fuel adjustment charges.' So the utility is incented to have the largest capital investment possible only balanced against the public perception of the associated rate request. Rate setting needs to change to better share the risk and therefore to incent utilities to reduce risk.

As we continue to see the change in energy risks and the perception of those risks, renewable energy will continue to expand and displace fossil fuels. Through discussion, education, and the evolution of our utility ecosystem, we can strive to accelerate and promote these positive changes for our environment and our economic competitiveness.

Comments